Policy Specific FAQs

Previous 11-15

As per section 129, the financial reporting requirements of Banking, Insurance, NBFC and Power companies are different from the Schedule III of the Companies Act, 2013, and thus, the applicable taxonomy for these companies are different from C&I Taxonomy (that is based on Schedule III).However, as the C&I Taxonomy 2015 is based upon reporting requirement as per Schedule III of the Companies Act, 2013, any exempted class of company that has prepared its Financial Statement as per Schedule III may voluntarily file in XBRL if it finds that appropriate taxonomy elements are available in the taxonomy.

The certification of XBRL filing would be done by the professional. The professional may use MCA XBRL Validation Tool to satisfy himself about the authenticity, accuracy and completeness of XBRL document vis-a-vis the audited financial statements of the company. Professionals may refer the Guidance provided by the professional institutes for certification of XBRL financial statements. MCA XBRL Validation Tool also provides for printable ‘human readable’ form of XBRL documents that may be used by professionals & companies to satisfy themselves about correctness of the filings.

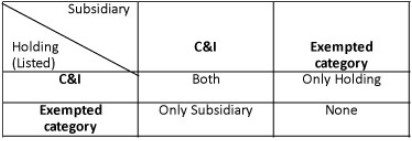

Yes, all Indian subsidiaries (including subsidiary of a subsidiary) of a listed company are mandated to file their financial statements in XBRL for FY 2014-15 onwards. It may be noted that listed holding company would provide subsidiary details in its standalone instance document, and its subsidiaries would separately file their financial statements in XBRL using e-forms AOC-4 XBRL

As per MCA circular, all companies who were required to file in XBRL mode in any of the earlier years are mandatorily required to file in XBRL mode this year as well. MCA recommends that a company which has done filing in XBRL mode last year on voluntary basis should continue to do so in subsequent years as well.